Page 33 - Plastics News June 2017

P. 33

FEATURES

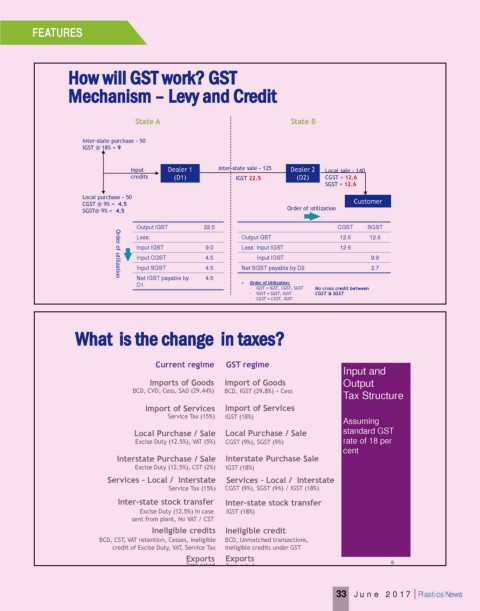

How will GST work? GST

Mechanism – Levy and Credit

State A State B

Inter-state purchase - 50

IGST @ 18% = 9

Input Dealer 1 Inter-state sale - 125 Dealer 2 Local sale - 140

credits (D1) IGST 22.5 (D2) CGST = 12.6

SGST = 12.6

Local purchase - 50

CGST @ 9% = 4.5 Customer

SGST@ 9% = 4.5 Order of utilization

Output IGST 22.5 CGST SGST

Less: Output GST 12.6 12.6

Input IGST 9.0 Less: Input IGST 12.6

Input CGST 4.5 Input IGST 9.9

Input SGST 4.5 Net SGST payable by D2 2.7

Net IGST payable by 4.5

Order of utilization

D1 • Order of Utilization:

- IGST = IGST, CGST, SGST No cross credit between

- SGST = SGST, IGST CGST & SGST

- CGST = CGST, IGST

5

* Calculations are made assuming GST of 18% for Goods and Services. Assuming State and Centre share equally

What is the change in taxes?

Current regime GST regime

Input and

Imports of Goods Import of Goods Output

BCD, CVD, Cess, SAD (29.44%) BCD, IGST (29.8%) + Cess

Tax Structure

Import of Services Import of Services

Service Tax (15%) IGST (18%)

Assuming

Local Purchase / Sale Local Purchase / Sale standard GST

Excise Duty (12.5%), VAT (5%) CGST (9%), SGST (9%) rate of 18 per

cent

Interstate Purchase / Sale Interstate Purchase Sale

Excise Duty (12.5%), CST (2%) IGST (18%)

Services – Local / Interstate Services – Local / Interstate

Service Tax (15%) CGST (9%), SGST (9%) / IGST (18%)

Inter-state stock transfer Inter-state stock transfer

Excise Duty (12.5%) in case IGST (18%)

sent from plant, No VAT / CST

Ineligible credits Ineligible credit

BCD, CST, VAT retention, Cesses, ineligible BCD, Unmatched transactions,

credit of Excise Duty, VAT, Service Tax ineligible credits under GST

Exports Exports

Zero rated Zero rated 6

33 June 2017 | Plastics News