Page 36 - Plastics News June 2017

P. 36

FEATURES

FEATURES

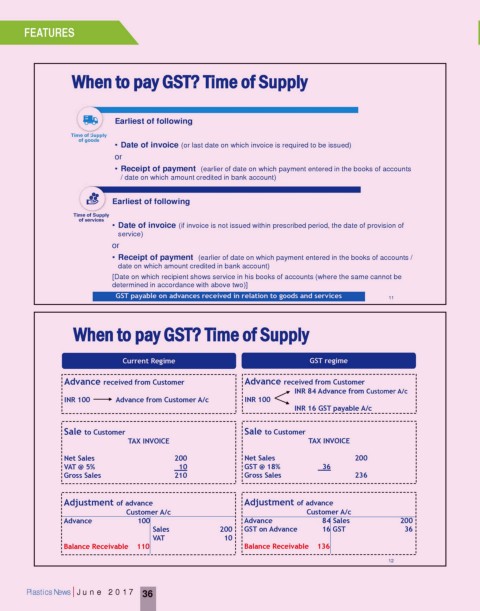

When to pay GST? Time of Supply

Earliest of following

Time of Supply

of goods

• Date of invoice (or last date on which invoice is required to be issued)

or

• Receipt of payment (earlier of date on which payment entered in the books of accounts

/ date on which amount credited in bank account)

Earliest of following

Time of Supply

of services

• Date of invoice (if invoice is not issued within prescribed period, the date of provision of

service)

or

• Receipt of payment (earlier of date on which payment entered in the books of accounts /

date on which amount credited in bank account)

[Date on which recipient shows service in his books of accounts (where the same cannot be

determined in accordance with above two)]

GST payable on advances received in relation to goods and services 11

When to pay GST? Time of Supply

Current Regime GST regime

Advance received from Customer Advance received from Customer

INR 84 Advance from Customer A/c

INR 100 Advance from Customer A/c INR 100

INR 16 GST payable A/c

Sale to Customer Sale to Customer

TAX INVOICE TAX INVOICE

Net Sales 200 Net Sales 200

VAT @ 5% 10 GST @ 18% 36

Gross Sales 210 Gross Sales 236

Adjustment of advance Adjustment of advance

Customer A/c Customer A/c

Advance 100 Advance 84 Sales 200

Sales 200 GST on Advance 16 GST 36

VAT 10

Balance Receivable 110 Balance Receivable 136

12

Plastics News | June 2017 36