Page 37 - Plastics News June 2017

P. 37

FEATURES

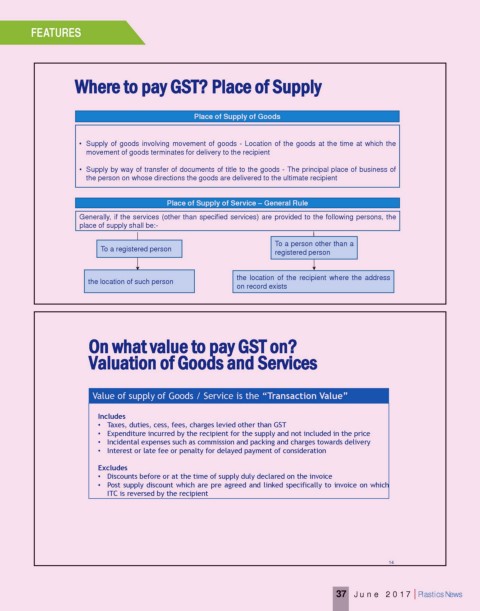

Where to pay GST? Place of Supply

Place of Supply of Goods

• Supply of goods involving movement of goods - Location of the goods at the time at which the

movement of goods terminates for delivery to the recipient

• Supply by way of transfer of documents of title to the goods - The principal place of business of

the person on whose directions the goods are delivered to the ultimate recipient

Place of Supply of Service – General Rule

Generally, if the services (other than specified services) are provided to the following persons, the

place of supply shall be:-

To a person other than a

To a registered person registered person

the location of the recipient where the address

the location of such person

on record exists

13

On what value to pay GST on?

Valuation of Goods and Services

Value of supply of Goods / Service is the “Transaction Value”

Includes

• Taxes, duties, cess, fees, charges levied other than GST

• Expenditure incurred by the recipient for the supply and not included in the price

• Incidental expenses such as commission and packing and charges towards delivery

• Interest or late fee or penalty for delayed payment of consideration

Excludes

• Discounts before or at the time of supply duly declared on the invoice

• Post supply discount which are pre agreed and linked specifically to invoice on which

ITC is reversed by the recipient

14

37 June 2017 | Plastics News