Page 40 - Plastics News June 2017

P. 40

FEATURES

FEATURES

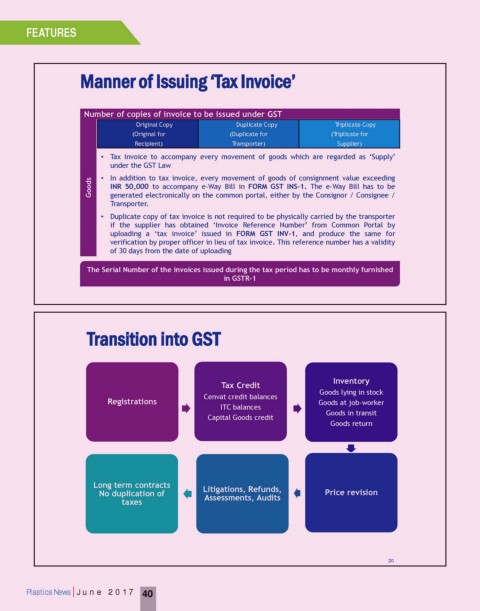

Manner of Issuing ‘Tax Invoice’

Number of copies of invoice to be issued under GST

Original Copy Duplicate Copy Triplicate Copy

(Original for (Duplicate for (Triplicate for

Recipient) Transporter) Supplier)

• Tax Invoice to accompany every movement of goods which are regarded as ‘Supply’

under the GST Law

Goods • In addition to tax invoice, every movement of goods of consignment value exceeding

INR 50,000 to accompany e-Way Bill in FORM GST INS-1. The e-Way Bill has to be

generated electronically on the common portal, either by the Consignor / Consignee /

Transporter.

• Duplicate copy of tax invoice is not required to be physically carried by the transporter

if the supplier has obtained ‘Invoice Reference Number’ from Common Portal by

uploading a ‘tax invoice’ issued in FORM GST INV-1, and produce the same for

verification by proper officer in lieu of tax invoice. This reference number has a validity

of 30 days from the date of uploading

The Serial Number of the invoices issued during the tax period has to be monthly furnished

in GSTR-1

19

Transition into GST

Tax Credit Inventory

Cenvat credit balances Goods lying in stock

Registrations Goods at job-worker

ITC balances

Capital Goods credit Goods in transit

Goods return

Long term contracts

No duplication of Litigations, Refunds, Price revision

taxes Assessments, Audits

20

Plastics News | June 2017 40